Projects

Bond Pricing & Yield Analysis

A static view of bond pricing analysis with pre-generated graphs and metrics.

This project is a Python-based Bond Pricing & Yield Analysis tool that applies discounted cash flow methods to price fixed-income securities and examine how bond values change as market yields move.

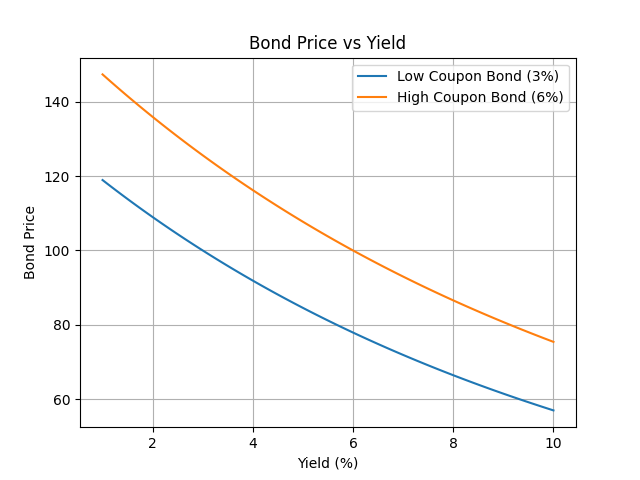

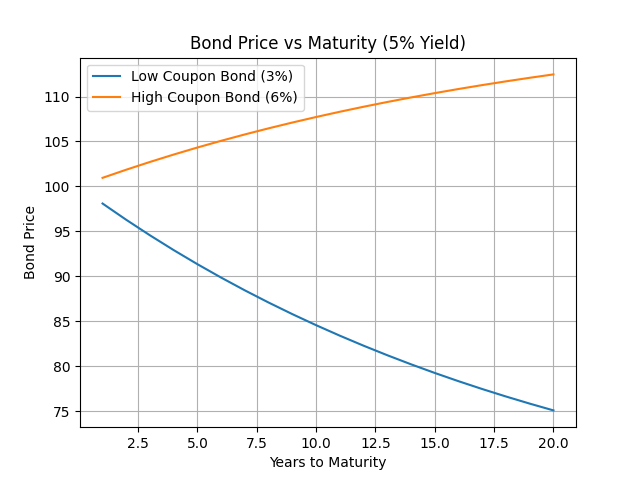

For this project, I focused on two example coupon bonds:

- Low Coupon Bond – a bond with a lower annual coupon rate, showing greater sensitivity to changes in yield.

- High Coupon Bond – a bond with a higher annual coupon rate, allowing comparison of pricing behaviour and interest-rate sensitivity.

The Python code calculates bond prices, Macaulay duration, and modified duration, and generates visualisations including bond price vs yield and bond price vs maturity. These plots help show the inverse relationship between bond prices and yields, as well as the effect of coupon rate and maturity on interest-rate risk.